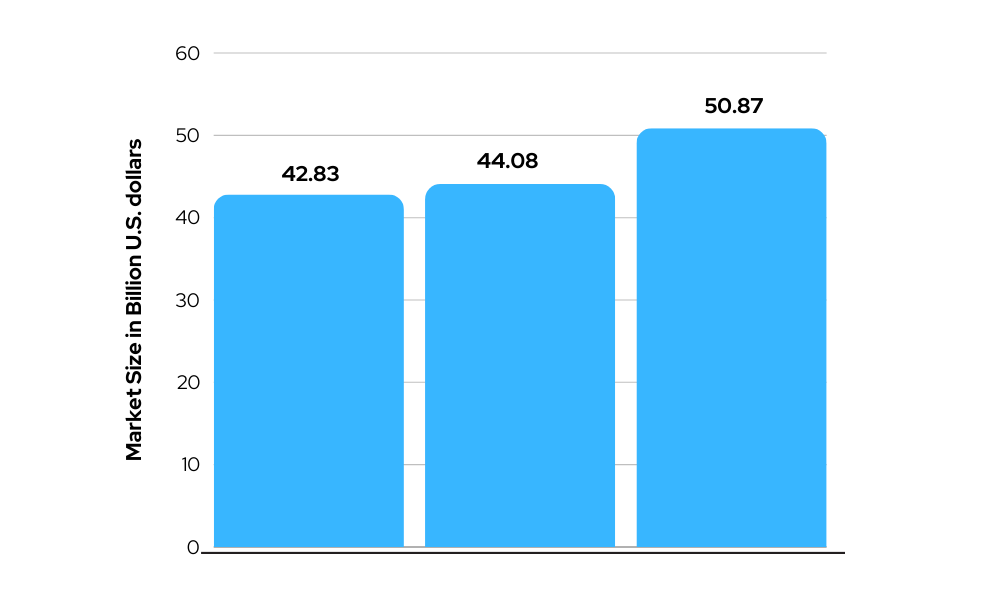

According to Statista, “The market size of artificial intelligence (AI) in fintech was estimated at 42.83 billion U.S. dollars in 2023, which grew to 44.08 billion U.S. dollars in 2024. With a compound annual growth rate (CAGR) of 2.91 percent, the market size is forecast to exceed 50 billion U.S. dollars in 2029.”

A major shift is occurring in the banking and financial services (BFSI) industry. It is no longer confined to the world of tangible branches and written pronouncements. These days, data and innovation are the driving forces behind this dynamic environment. Artificial Intelligence (AI) is at the vanguard of this revolution, with the potential to take the sector to unprecedented heights by 2024 and beyond.

The foundation of a strong global economy is the banking and financial services (BFSI) industry. Financial institutions are essential for managing risks, enabling investments, and simplifying transactions. Nonetheless, the sector is often confronted with difficulties, such as fierce rivalry, changing laws, and the growing need for customization. Artificial intelligence (AI) becomes a game-changer in this situation.

This article delves into the critical role AI plays in the Banking and Financial sector. We’ll explore the current issues facing financial services, the fundamental importance of this industry, and the defining characteristics that make it ripe for AI integration. We’ll then delve into the transformative power of AI, showcasing its applications and the potential benefits it unlocks for both institutions and customers. Finally, we’ll touch upon some considerations and ethical dilemmas surrounding AI in finance.

The Role of AI in the Financial Services Industry

Artificial Intelligence (AI) includes a variety of technologies, such as computer vision, machine learning, and natural language processing, that allow machines to mimic human intelligence. Artificial Intelligence (AI) is being used in the Financial Services Industry (FSI) to boost security, automate procedures, and customize consumer experiences.

Automation and Efficiency: AI has the potential to automate processes, allowing for the simplification of tedious work and the enhancement of FSI procedures. Financial organizations may automate back-office tasks like data input, document processing, and regulatory compliance by implementing AI-powered algorithms. FSI companies may save a lot of money, increase operational effectiveness, and reallocate human resources to more high-value work by using AI for automation.

Enhanced Decision-Making: The potential of AI to improve decision-making processes in the FSI is among its most important benefits. Large data sets can be analyzed by machine learning algorithms, which can also spot trends and produce useful insights for making strategic decisions. Predictive analytics powered by AI, for example, can assist financial organizations in predicting market trends, evaluating credit risk, and customizing investment strategies. FSI professionals may make data-driven decisions with more confidence and precision by utilizing AI for decision support, which will ultimately spur business expansion and profitability.

Personalized Services: Financial organizations may provide individualized services based on the demands of each individual consumer thanks to AI. AI is able to provide individualized financial product, service, and investment recommendation by examining consumer data and behavior. Financial institutions profit more from this tailored strategy since it increases consumer happiness and loyalty.

Risk Management and Fraud Detection: In the financial services sector, artificial intelligence is essential to fraud detection and risk management. Large volumes of data may be analyzed by machine learning algorithms, which can then be used to instantly spot fraudulent activity and identify possible threats. By taking a proactive stance, financial institutions can reduce risks and safeguard their clients from fraud.

Regulatory Compliance: The financial services sector places a high priority on regulatory compliance, and artificial intelligence (AI) can help to expedite compliance procedures. Systems driven by AI are able to keep an eye on transactions, spot questionable activity, and guarantee that rules are being followed. Financial institutions save time and money because to this automation, which also lowers the risk of non-compliance.

Customer Insights and Market Trends: AI can give important insights into consumer behavior and industry trends. AI has the potential to improve financial organizations’ understanding of client demands and preferences by evaluating data from a variety of sources, including social media. With this knowledge, creative goods and services as well as focused marketing efforts can be created.

Benefits of AI for Banking and Financial Services

The implementation of AI in banking offers numerous benefits for both financial institutions and their customers:

Cost Savings: Artificial Intelligence (AI) in banking can result in significant cost savings by eliminating the need for human participation in a number of procedures. Financial organizations may save operating expenses by using AI-powered solutions to automate processes like data entry, customer support, and fraud detection.

Enhanced Security: AI can enhance banking security protocols by instantly identifying and stopping fraudulent activity. By analyzing trends in transaction data, machine learning algorithms can spot possible fraud and help banks safeguard the assets and personal data of their clients.

Streamlined Operations: AI can automate workflows and repetitive tasks, which will streamline banking operations. Reduced mistakes, quicker transaction processing times, and more overall efficiency can all result from this automation.

Improved Compliance: Artificial Intelligence (AI) has the potential to enhance banks’ regulatory compliance by automating compliance operations and keeping an eye on transactions for questionable activity. By doing this, financial institutions may be less likely to violate the law and face penalties.

24/7 Availability: Artificial intelligence (AI)-driven chatbots and virtual assistants can offer customer service and support around-the-clock, increasing accessibility and making sure that customers’ needs are satisfied at all times.

Predictive Analytics: AI can assist banks in using data to forecast consumer behavior, industry trends, and possible hazards. This can help banks find new business opportunities, proactively address consumer requirements, and reduce hazards before they become more serious.

Challenges and Considerations for AI in Banking

Despite its numerous benefits, implementing AI in banking also presents certain challenges:

Data Privacy and Security: Concerns around data security and privacy arise because implementing AI in banking necessitates access to enormous volumes of consumer data. Banks need to make sure AI systems follow data privacy laws and put strong security measures in place to safeguard client data.

Algorithmic Bias: Unintentionally maintaining biases found in the data that AI algorithms are educated on can produce unfair or biased results. In order to reduce the potential of algorithmic bias, banks must carefully build and monitor AI systems.

Explainability of AI Decisions: Explaining AI-driven judgments can be challenging, particularly in cases when consumers are turned down for loans or other financial services. To keep customers’ trust, banks must guarantee openness and give concise justifications for AI judgments.

Job Displacement and Workforce Reskilling: AI-driven automation has the potential to eliminate jobs in the banking industry. In order for banks to meet the evolving needs of AI-driven banking, they must devise plans for retraining and reskilling their personnel.

Ethical and Legal Considerations: When implementing AI in banking, banks must take into account the ethical and legal ramifications, including concerns about prejudice, discrimination, and fairness. In order to employ AI ethically, banks must set clear policies and standards and make sure that all applicable laws and regulations are followed.

Continuous Monitoring and Improvement: To guarantee their efficacy and dependability, AI systems in banking need to be continuously monitored and improved. Establishing systems to track AI performance, identify problems, and apply updates and enhancements as required is crucial for banks.

Final Thoughts

In summary, by 2024, artificial intelligence will have drastically changed the banking and financial services sector. Artificial Intelligence (AI) is bringing about a more efficient, secure, and customer-focused environment by automating tasks and personalizing customer interactions.

Collaboration is essential, though, if this shift is to realize its full potential. To guarantee the responsible development and application of AI, banks must collaborate closely with regulators, technology providers, and consumer advocacy organizations. Establishing trust and addressing issues related to data privacy, algorithmic bias, and the explainability of AI choices would require open communication and transparent procedures.

Artificial intelligence in banking will not take the place of human knowledge. Rather, the focus is on establishing a potent combination of human and artificial intelligence. AI can take on the labor-intensive duties of automation and data analysis, freeing up human workers to concentrate on jobs that call for empathy, creativity, and sophisticated problem-solving. In order to provide individualized financial advice, build stronger customer relationships, and navigate the always shifting financial landscape, human-AI collaboration will be essential.